8 min read

How Young Fintechs Surpass Their Competitors’ CX to Achieve FI Traction

How Young Fintechs Surpass Their Competitors’ CX to Achieve FI Traction

Understanding how the unique CX challenges for fintechs in the ‘Achieve Traction’ stage of the product lifecycle impact FI sales

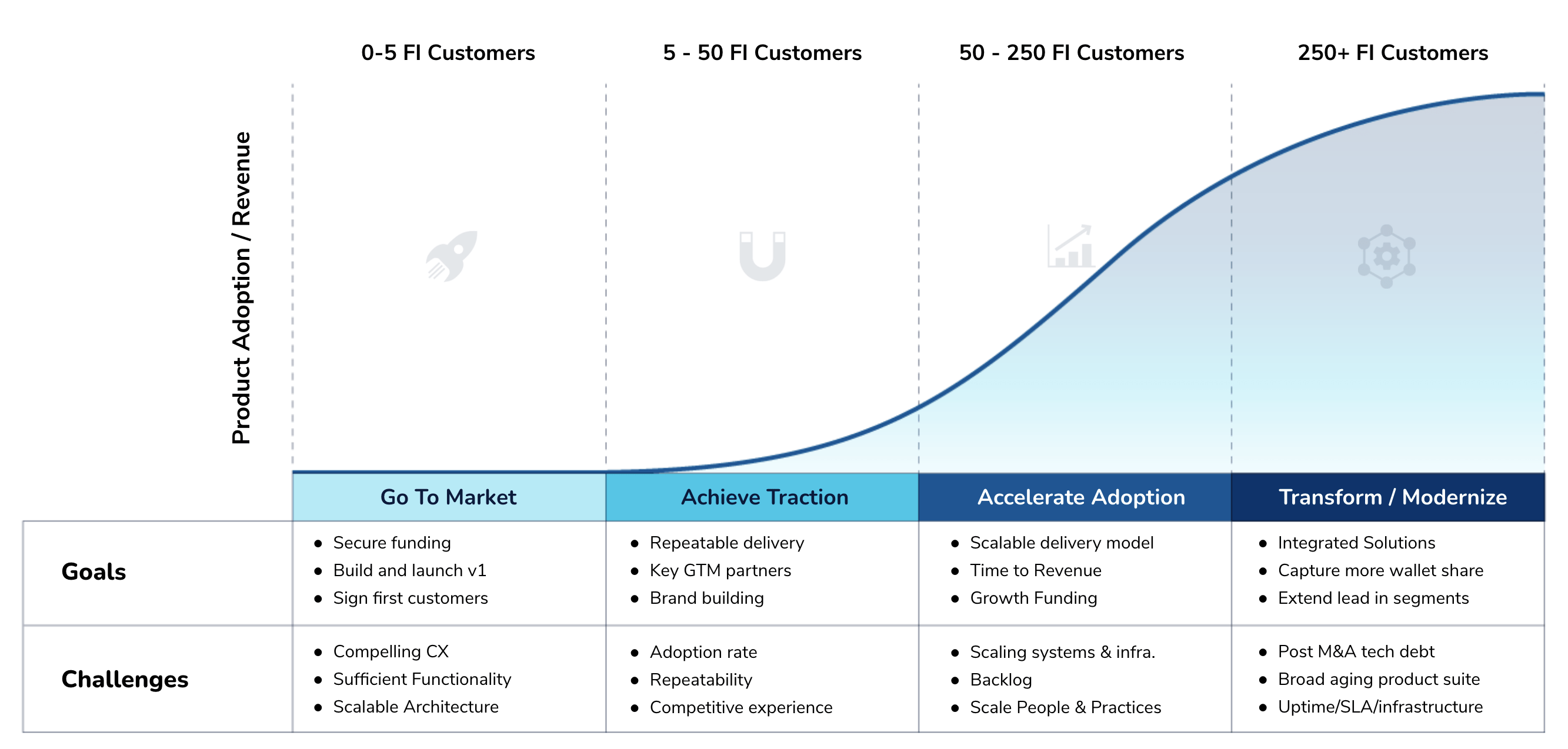

Every fintech product can be said to fit into a particular stage of the software adoption lifecycle. Fairly new fintechs just finding their trajectory, facing increasing but unpredictable sales are in the Achieving Traction stage. Fintechs at this stage are landing some customers, yet still losing most of their deals and are just starting to find their product-market fit. In order to build on their wins and mature as a company, a product at this stage must implement some basic capabilities to level up.

The CX Challenges of Achieve Traction Stage Products

A lack of integrations with other fintech products and legacy systems via ecosystem partnerships, or core integrations is one common challenge to fintechs still trying to achieve traction on their product-market fit. Relatedly, fintechs at this stage may also be limited in terms of their product’s customization and configurability — but are also keenly aware of the need for deeply personalized CX.

The issue they face is blinkered vision, having worked internally on their product for so long, a general lack of awareness of digital CX weak points manifests itself. These natural blindspots can lead to poor business outcomes – poor conversion rates, poor retention, and slow acquisition. Looking past their blindspots, competitive young fintechs recognize the market demand and expectations for CX are consistently increasing — hence the fiercely competitive sales environment amongst fintech software providers.

Solutions Used to Address CX Challenges – And Their Outcomes

Many fintechs rely heavily, even entirely, on their internal teams and/or existing software development partners to help fill in the gaps ad-hoc. Between limited funds and the need for domain expertise, this is often seen as the only solution for early stage fintechs. However, product executives we’ve worked with warn that relying on internal teams alone can slow the process, leading to missed revenue targets. Further, an ad-hoc response to CX issues typically compounds itself, resulting in slow deployment and large backlogs. And for those who turn to their software development partners, while initially convenient, this can often manifest in poor product differentiation. When this happens, they receive an increase in client complaints about the lack in customization and brand support. It’s a fix, but is it a truly customized, exceptional CX? Likely not if the product resembles the clients’ competitors’.

Taking a different approach, other fintech leaders may end up hiring expensive consultants who, in many cases are stellar strategists, often don’t have ‘boots on the ground’ knowledge to actually execute on the strategies that they recommend. For a development team to succeed, they need a rock-solid strategy — one that includes in-depth implementation support and guidance. When a consultant can’t fully deliver on this need, the result is usually a high-cost, impractical, unrealized CX solution. The momentum needed to shift a new fintech product from pre-revenue to highly competitive is just not quite there without that critical combination of CX strategy and development skills — and this disconnect results in suboptimal business and technical impacts.

No matter the approach to CX challenges, fintechs across the entire software adoption lifecycle will find that some solutions amount to little more than front-end band aids. These quick, cosmetic fixes don’t address deep, holistic CX issues and often result in technical and design debt. But the worst resolution? Giving into misalignments between business and technical teams and doing nothing at all. Fintechs that avoid their CX issues ultimately push the problem onto the FI client, making a product the opposite of a valued response to a market need. The ripple effect is profound, impacting the clients’ customers, and coming back around to impact the fintech in the form of unhappy clients, reputational damage, underwhelming adoption rates, and high loss rates for new sale opportunities.

A Better Solution

Top performing fintech leaders look at CX as their key competitive differentiator by addressing it in a more holistic way, including:

- Customizations that support personalized CX and FI brand support

- Understanding and addressing how both FIs and consumers use and engage with the product

- CX as a function of system performance, stability and scalability across the entire ecosystem

- Alignment between internal business and technical stakeholders

- How to identify and track key metrics for CX success

- Engaging neutral third party experts with empirical frameworks to analyze their core product CX

In order to gain the competitive edge, a fintech product requires a better digital CX than its competitors. Successful fintechs take a broader perspective and incorporate insights from competitor products too. Innovative product leaders require more than an intimate knowledge of their own products — if that alone was enough, there would be no need to hone in on market fit in the first place. Acknowledging that their internal teams are fraught with competing voices, misaligned understandings of the priorities, and have limited bandwidth for collecting the external perspectives of both financial institutions on the market for their products and their competitors, they rely on external expertise. Praxent offers deep CX expertise, specializing in fintech products.

Our Approach

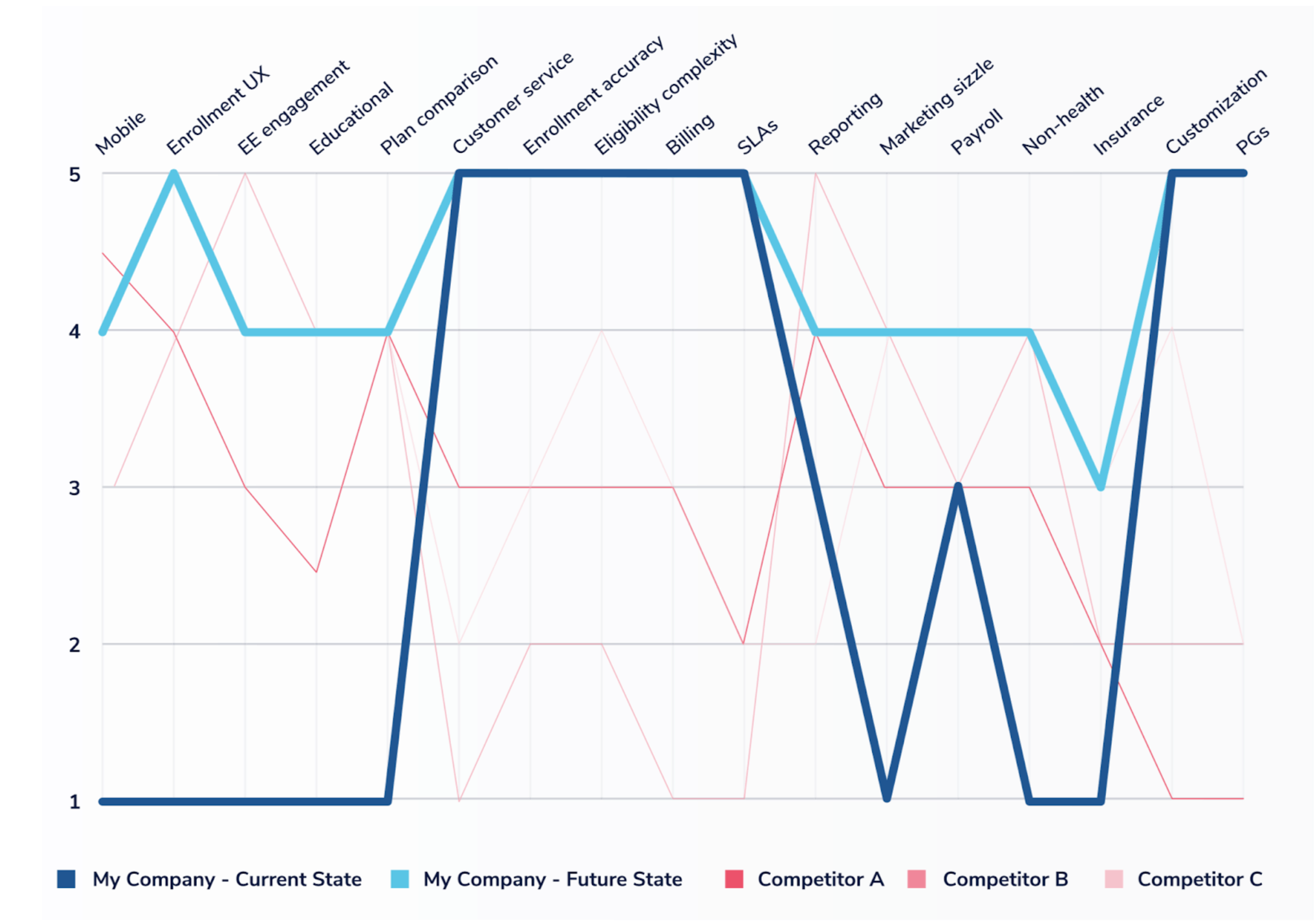

With an outside perspective that’s rooted in fintech domain expertise — and hundreds of successful CX projects — Praxent conducts deep Competitor Comparison Audits for our fintech clients.

Taking a look at the wider market, comparing against the competitors, and allowing clients to see where the gaps are that are losing them sales. In a Competitor Comparison Audit:

- Praxent CX experts analyze the product against 5 competitors, reviewing their features, benefits, and customer journey, and customer experience.

- The findings are compiled into a detailed report with prioritized recommendations for improving the product’s CX competitiveness.

Customer Journey Maps are an alternative solution. A CJM outlines the process our client’s customer goes through to acquire value from the company. It includes:

- A listing of the touch points, the steps along the way, at which a company delivers value,

- What is required in order to deliver that value, and the corresponding frustrations and delights customers experience as they seek to achieve it.

- Praxent CX experts then compare this to competitor companies to discover the gaps.

When fintechs product owners lay out their customer’s journey from end to end, they gain valuable insights that can help fix the CX gaps now and make better product decisions later.

The Results

An approach rooted in an impartial, expert third party audit results in an exceptional customer experience. When the insights revealed in an audit are implemented to catalyze change, young fintechs experience a faster time to market and smaller backlogs — gaining focus on making the most impactful changes, and nothing else.

With a competitor audit in hand, product leaders are able to improve business and technical alignment, leading to faster product roadmap execution. With a newly CX-competitive product, they see faster customer acquisitions, increased adoption, higher conversion and retention rates — and their FI clients report higher customer satisfaction rates. They enable their clients to have customized experiences that support their branding, their unique workflow needs, and maintain a consistently high quality CX as consumers traverse systems. This translates to more robust integrations — and more growth.

“Analyzing the user experience of your competitors is so valuable. It allows you to benchmark your company and find opportunities to differentiate across a variety of attributes such as color usage, content structure, design features, and general aesthetic. It’s a low-hanging fruit activity that gets the design gears turning quickly.”

– Praxent Associate Director of Design – Nick Comito

Interested in learning where you stand against the competition? Talk to a Praxent expert about how your fintech can implement a competitor CX audit and overcome the CX excellence gap that’s holding your back from growth

Speak to an expert

Leave a Reply