9 min read

Fight, Flight or…Freeze? How Aging Fintechs Can Get Unstuck and Transform Their CX

Fight, Flight or…Freeze? How Aging Fintechs Can Get Unstuck and Transform Their CX.

Understanding how the unique CX challenges for fintechs in the ‘Transform/Modernize’ stage of the product lifecycle impact FI sales

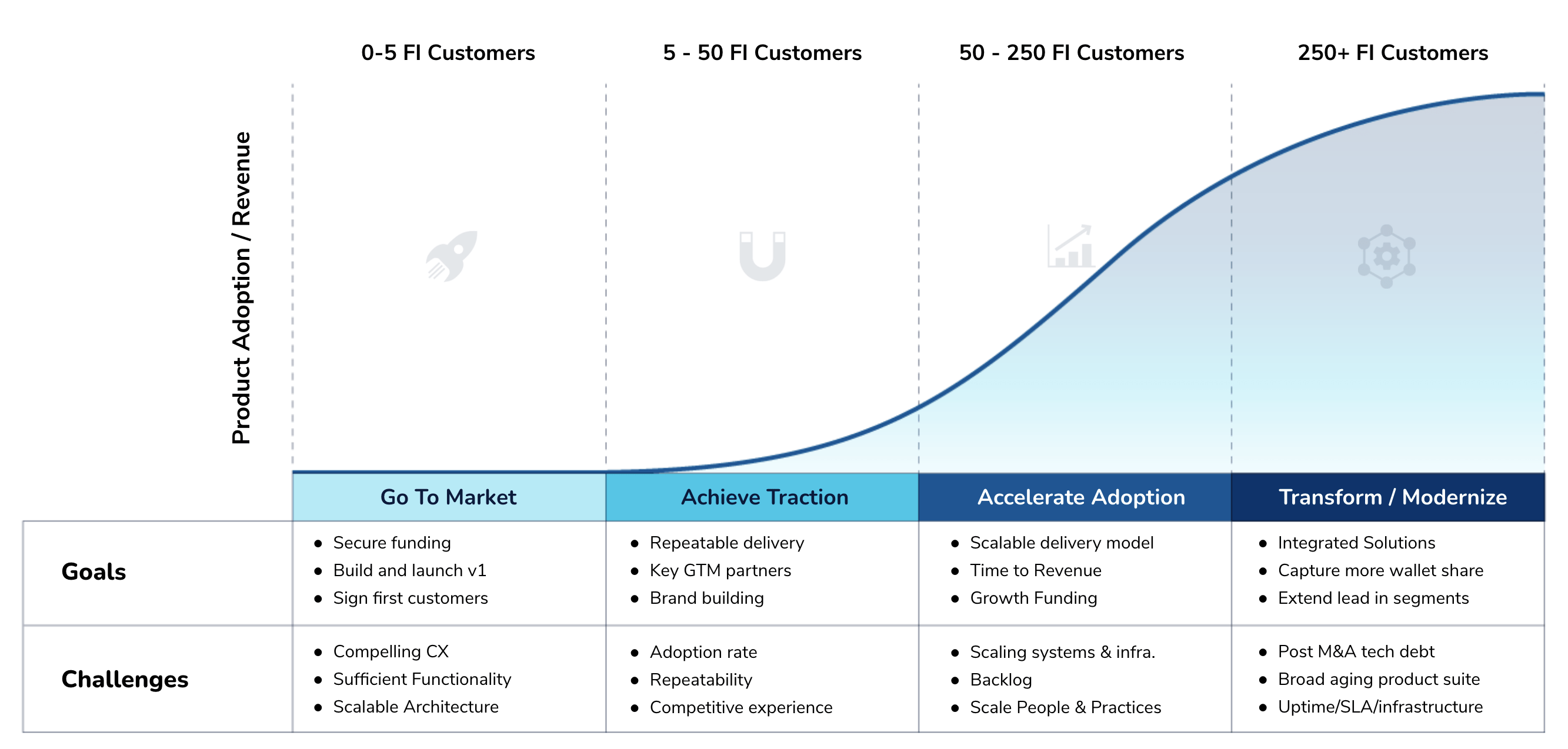

An established fintech has been in the game for some time and has found a solid product-market fit that has enabled them to beat out their competitors. A fintech at this stage is no stranger to technical and design debt — in order to get their product and acquisitions to market, they’ve made quick fix patches time and again. A competitive edge drives them, but let’s face it — it can sometimes be to the detriment of the product. At this stage in the game, a fintech product might even be considered a legacy product. This stage of the software adoption lifecycle is known as the Transform/Modernize stage because they’re now at a crossroads — either transform or modernize their product, or risk decaying.

The CX Challenges of Transform/Modernize Stage Products

When Praxent has spoken with deeply experienced fintech product leaders — especially those with legacy products — they know that at their stage of maturity, their digital CX often leaves something to be desired. Fintech leaders at this stage are highly aware of the increased drive towards personalization and customization, but limited in terms of just how readily they can reconfigure their products to fit customers’ expectations. This can translate as outdated, sometimes clunky applications that are far from seamless (not to mention that mounting technical and design debt). As a result, they may be experiencing a declining trend in sales and customer retention. Fintechs who are in this critical stage know the time to invest in transformation is at hand — or further decay will be the inevitable outcome.

Further challenge lies in the complexity of the relationships these leaders have built via their products– all those integrations with other fintech products and legacy systems via M&A, ecosystem partnerships, or core integrations are complicated and must be taken into consideration when undergoing a major software transformation. And with limited implementation partners who are skilled enough to deliver a customized digital CX for financial institutions on their behalf, winning trust may also be a challenge.

With the extremely competitive sales environment amongst fintech software providers today, product executives recognize their challenge clearly: to raise the bar of excellence for digital CX higher. When Praxent speaks with product leaders, they often express the need to be able to make a transformative CX upgrade and increase their design capacity in order to get competitive features to market quickly. The key is to do so while also eliminating technical and design debt.

Solutions Used to Address CX Challenges – And Their Outcomes

When faced with the choice to either transform or decay, fintechs at the stage tend to hit fight, flight, or freeze mode. Freeze mode happens when business and technical teams are misaligned internally. Unsure or in conflict about how to solve the CX problem, the entire organization becomes stuck in the mud, seemingly unable to move forward and do things differently. When nothing changes, this results in essentially pushing off the problems to the financial services customers. And when the customers are left bearing the weight of an outdated product, customers feel it too. The circle of life from a CX perspective leaves no party untouched.

Another response is to enter flight mode — opting to hire on expensive outside consultants who appear well-versed in CX — but critically, lack understanding of fintechs and financial services, and hence cannot adequately solve the unique digital CX challenges a decaying fintech faces. When a fintech is in flight mode, a lack of design consistency, customization, and brand support becomes apparent — and the customers, once again, take notice.

When a fintech chooses fight mode in their battle to address major CX challenges, they’re typically doing the best they can given the resources they have at hand. This may consist of deploying internal teams in a sometimes scattered approach — ad hoc responses to temporarily fill in critical gaps, establishing cross-functional internal task forces, relying on an existing software development partner, or calling on third party partners to execute on customized solutions and deployments.

This fight, while commendable, also results in suboptimal outcomes. Distracting core development and engineering leadership from product roadmap items, long and expensive development cycles with limited end results, slow deployments, large backlogs, and yes — unhappy, underwhelmed customers. All this manifests as high support load and expense, high internal or external labor costs, extended time to value for acquired assets, higher customer churn rates, and missed revenue targets. The people behind the product just know it could perform better — but it’s not, and that’s making an impact on stakeholder relationships and company reputation.

A Better Solution

If a fintech finds itself at this stage, then doing things the usual way amounts to little more than ignoring the market demand for digital CX excellence. Praxent has met with teams simply too overwhelmed and deep in the weeds to see their problems clearly — and this is often the case even when things appear to be going well. Innovative fintech leaders realize that they don’t have to go it alone — but their standards are high, requiring fintech CX specialists with established, industry-specific design practices so as not to waste time bringing them up to speed on domain knowledge.

When looking at potential third party partners, a fintech should ensure that they support:

- Customizations that support both personalized CX and FI brand support

- Understanding and addressing how both FIs and consumers use and engage with the products

- CX as a function of system performance, stability and scalability across the entire ecosystem

- Alignment between internal business and technical stakeholders

- Identifying and tracking key metrics for CX success

- Utilization of empirical frameworks to analyze product CX

- Consistency in CX design best practices

To make truly transformative upgrades, an established fintech needs an external perspective capable of helping redirect alignment with their team around how to get unstuck. This will enable them to either take control of their legacy product before it starts declining — or to reimagine the entire experience and modernize the product to be more consistent with current standards and regulations. This is where Praxent can help.

Our Approach

Praxent conducts Holistic CX Audits so that product leaders can obtain objective, deep, multilayered, assessment of their products’ existing CX. We also provide logical next steps for going forward, ensuring their CX is led by design best practices so they can improve:

- Intuitiveness and ease of use

- User focus on the conversion

- Personalization and customization

- User brand support guidance

- Consistency of CX design in order to increase trust with users

During the Holistic CX Audit process, Praxent will audit and assess a user workflow, even if it’s across multiple products, according to heuristic design best practices. We’ll then create a report detailing each opportunity for improvement and a prioritized list of recommendations for a design team to tackle in order to improve the CX of their product.

The Results

In taking this holistic approach, fintechs are enabled to achieve an elevated customer experience that includes:

- A true out of the box experience for FI users and consumers, making sure the core fintech product is optimized for excellence in CX

- Customized experiences for FIs and their consumers, Enabling FIs or direct consumer users to have customized experiences that support their branding, unique workflow needs, and create competitive differentiation

- Maintaining a consistent and high quality CX as users traverse fintech back end systems and integrations with good speed, availability, stability and scalability.

Transformations rooted in a heuristic understanding of the core CX issues at hand dramatically impact conversion rates, drop rates, support load, and customer satisfaction. With transformation supported by Praxent’s fintech CX design experts, companies also experience less distracted core teams, higher engineering efficiency, smaller backlogs, product roadmap execution, and better long term system performance. This can translate to better retention, faster new customer acquisition, and ultimately, a more competitive, modernized product.

What Praxent Clients Have to Say:

“We have an internally built customer-facing portal where our customers access data. Even though the platform itself was homegrown in terms of its functions, we worked with Praxent to really dig into and help us understand the psychological effects of the design and technologies that we were using, as well as how those were affecting the human interactions being driven through the platform.

We have a fairly unique position within the market, so their first task after we brought them on was really to try to understand our customers, and then from there they were able to take our existing platform, perform a true heuristics evaluation, and break down how it needed to be redesigned in a lot of different ways.”

– Senior Business Development Analyst, EDF

Interested in exploring how a Holistic CX Audit can help transform your CX? Talk to an expert about how your fintech can take control of your product today.

Speak to an expert

Leave a Reply